Key Concepts Study Tool: Chapter 18

Click on each concept below to check your understanding.

1. Influential Cases as a Source of Error

- Any case that exerts an extraordinary amount of influence on the slope and intercept.

- There are two types of influential cases:

- Outlier: the distance an observation is from its estimated Y-value (the distance between Yi and ŷ is huge)

- Leverage: measures the distance between an X-value and the mean for that variable (the gap between Xi and x̄)

2. Cook’s Distance (Cook’s D)

- Introduced in the late 1970s by Dennis Cook.

- Determines the extent to which coefficient estimates (both slopes and intercepts) will change if a particular observation is removed from the analysis.

- Values are meaningless by themselves, but any value below 1 is regarded as being tolerable for influence.

- Any observation exceeding 1 should be examined closely and possibility deleted.

3. Heteroscedasticity as a Source of Error

- Homoscedasticity: examined by looking at the distribution of estimation errors (the difference between the predicted Y’s and the actual y’s) across X-values.

- A regression is considered homoscedastic if the standard deviation of the estimation error for each value of X is roughly similar. If that condition is not met, the model is heteroscedastic.

- When the condition of homoscedasticity is not met, the accuracy of that coefficient can be question.

- The easiest way to detect heteroscedasticity is to look at a residual versus a fitted value plot.

4. Multicollinearity as a Source of Error

- Collinearity, or multicollinearity, is found when independent variables share a common line when graphed. In other words, they are correlated.

- When collinearity is strong, identifying the independent impact of X1 will be difficult, because whenever variable Y is increased by one increment, so is X2. Finding the independent impact of either variable is virtually impossible because they are so intertwined.

- When any two independent variables are correlated at 0.5 or above, it is important to examine them.

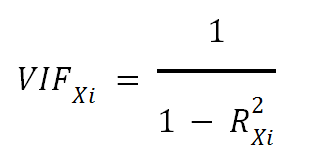

5. Identifying and Dealing with Multicollinearity

- To identify multicollinearity the variance inflation factor (VIF) is computed for each variable.

- VIF values that exceed four are generally worthy of further investigation.

- Options for dealing with multicollinearity include: dropping one of the collinear variables, or combining the two offending variables to form one composite measure. The latter option may not make sense in every situation.